Navigating Financial Conversations with Aging Parents

Having a conversation with your parents about their finances can seem like a daunting task. However, it is an essential step in helping to ensure their financial well-being as they get older. Here are some practical tips to help you navigate these discussions.

Start the conversation

Talking about money can be difficult. However, it's important to initiate a financial conversation with your parents before they become too ill or incapacitated. Your parents may be unwilling to talk to you at first because they are reluctant to give up control over their financial affairs, or they are embarrassed to admit that they need your help. It's important to approach the topic sensitively and make it clear that you fully respect their needs and concerns.

If they are still hesitant to talk to you and are capable of managing their affairs for now, you may want to revisit the discussion later. Or you could suggest that they talk to another family member, trusted friend, attorney, or financial professional.

Organize financial and legal documents

Once the lines of communication are open, you can help your parents organize their financial and legal documents. Start by creating a personal data record that lists the following types of information:

- Financial: Include all of your parents' bank/investment account information, including account/routing numbers and online usernames and passwords. You should also list any real estate holdings, along with any outstanding mortgages. Do your parents receive income from Social Security, a pension, and/or a retirement plan? You will want to include that information as well.

- Legal: Find out if your parents have had any legal documents drawn up, such as wills, trusts, durable powers of attorney and/or health-care directives. Locate other important documents too, such as birth certificates, property deeds, and certificates of title.

- Medical: Determine what type of health insurance your parents have — Medicare, private insurance, or both. You should also have the names and contact information for their health-care providers, their medical history, and any current medications.

- Insurance: List what other types of insurance coverage your parents have — life, home/property, auto, or long-term care, for example — along with the names of their insurance companies and policy numbers.

Store the data record and any other pertinent documents either electronically or in a secure, fireproof box or file cabinet.

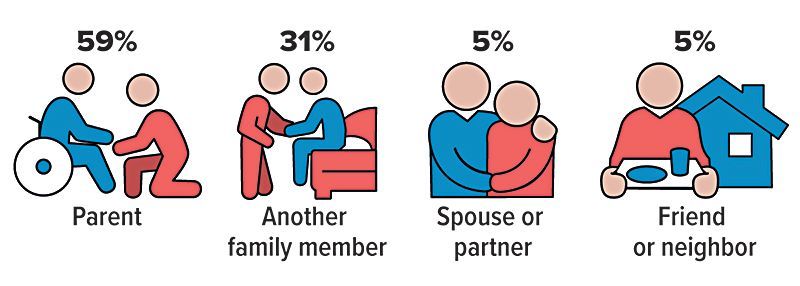

Who Are Caregivers Caring For?

Help with managing finances

You can help your parents manage their finances by examining their budget and finding out their monthly income and expenses. Track your parents' spending to make sure that they are living within their means. You should also discuss ways to address any outstanding debts they may have.

Find out how your parents pay their bills and expenses. If they still use traditional methods, encourage them to set up safer and more convenient ways to bank such as direct deposit and making payments online, instead of mailing paper checks. If your parents are uncomfortable with electronic payments, remind them to mail all bills inside the physical post office and not to use outdoor mailboxes, which may be targets for mail theft.

Do your parents need additional support in managing their finances? There are ways for you to obtain the necessary authorization to assist them. One way is to become a joint account holder on certain bank accounts. This can give you direct access to manage transactions, monitor account activity, and ensure bills are paid. However, being a joint account holder may have certain legal and tax ramifications. Another option is for them to obtain a durable power of attorney, which is a legal document that grants you authorization to make financial decisions on their behalf, even if they become incapacitated. It may also be helpful for them to add you or someone else as a trusted contact for their accounts.

Discuss estate planning issues

If they haven't already done so, make sure your parents have certain legal documents in place — such as wills and/or trusts — to ensure that their estate planning wishes are followed. In addition, they may need to have a durable power of attorney, health-care proxy, and living will in place so they have someone to manage their money and health-care issues if they become ill/impaired. Issues surrounding the care of an aging parent can be complex. Consider consulting a financial professional and/or elder law attorney who specializes in financial and legal issues that affect older adults.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.