What Is Asset-Based LTCI?

When planning for the potential cost of long-term care, you've probably considered long-term care insurance (LTCI).

But premiums can be expensive, and if you do buy the coverage, you probably hope you never have to use it. The prospect of paying costly premiums for long-term care insurance that you may never use might discourage you from buying coverage.

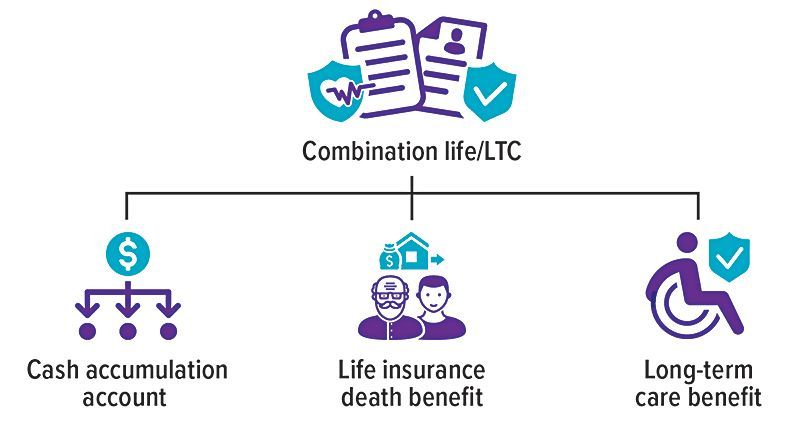

A possible solution is a type of insurance that blends several types of insurance coverage into a single policy. These hybrid LTC policies, also known as asset-based plans, combine the benefit of a life insurance policy or an annuity with the availability of long-term care benefits should you need them.

Life insurance asset-based plan

This type of plan combines permanent life insurance and long-term care coverage. Many such policies often require a substantial up-front premium, although some policies offer periodic premium payments (e.g., monthly, quarterly, annually). The amount of death benefit and long-term care allowance is based on your age, gender, and health at the time you buy the policy.

The appeal of this combination policy is that either you'll use the policy to pay for long-term care expenses, or your beneficiaries will receive the insurance proceeds at your death. In either case, someone will benefit from the premiums you pay. Benefits under an asset-based life insurance policy typically begin when the insured needs help with two or more activities of daily living such as eating, bathing, and dressing.

Annuity asset-based plan

While policy provisions may differ from company to company, generally you put money into an annuity, usually in a lump sum or through a series of premium payments. You may also exchange another annuity or cash-value life insurance for a long-term care annuity via a Section 1035 exchange. The annuity typically pays a fixed rate of interest each year. In addition, the annuity provides a long-term care benefit amount, usually equal to two or three times your annuity cash value, subject to a maximum benefit period, which is the maximum length of time that you may receive long-term care benefit payments from the annuity.

Long-term care annuity benefits are often paid monthly. There is usually a charge for the long-term care component that is deducted from your annuity each year. With this type of plan, you can use the annuity proceeds for long-term care, and if you don't use the long-term care benefit, you still have the typical annuity options (tax-deferred savings, lifetime income payments, etc.).

Whether an asset-based plan is right for you depends on a number of factors. But an asset-based plan may be a viable option available for long-term care planning that might merit a second look.

NOTE: Permanent life insurance offers lifetime protection and a guaranteed death benefit as long as you keep the policy in force by paying the premiums. A portion of the permanent life insurance premium goes into a cash-value account, which accumulates on a tax-deferred basis throughout the life of the policy. Withdrawals of the accumulated cash value, up to the amount of the premiums paid, are not subject to income tax. Loans are also free of income tax as long as they are repaid. Loans and withdrawals from a permanent life insurance policy will reduce the policy's cash value and death benefit and could increase the chance that the policy will lapse, and might result in a tax liability if the policy terminates before the death of the insured.

Generally, to be considered a tax-free exchange rather than a taxable surrender, you cannot receive the annuity proceeds directly; the proceeds from the annuity must be paid directly to the long-term care insurance company. Also, Section 1035 applies only if both the annuity contract and the long-term care insurance policy are owned by the same person or persons. A complete statement of coverage, including exclusions, exceptions, and limitations, is found only in the long-term care policy. It should be noted that carriers have the discretion to raise their rates and remove their products from the marketplace.

Generally, annuity contracts have fees and expenses, limitations, exclusions, holding periods, termination provisions, and terms for keeping the annuity in force. Most annuities have surrender charges that are assessed if the contract owner surrenders the annuity. Withdrawals of annuity earnings are taxed as ordinary income. Withdrawals prior to age 59½ may be subject to a 10% federal tax penalty. Any guarantees are contingent on the claims-paying ability and financial strength of the issuing insurance company.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.