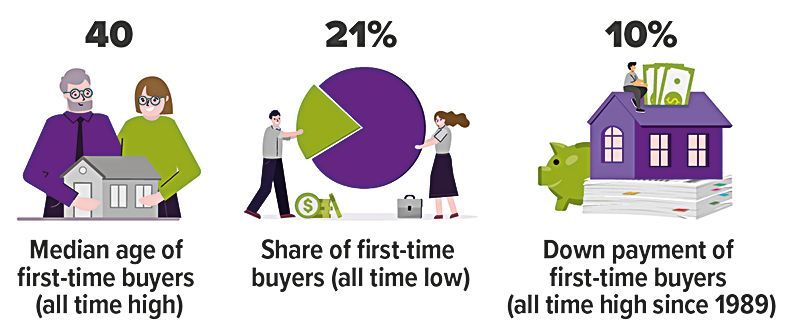

Locked Out? How to Break Into Today's Housing Market

For many young people today, the prospect of buying a home can seem out of reach.

High prices, elevated interest rates, and limited inventory all make the current housing market a challenging one. Fortunately, homeownership can still be an attainable goal. It may just take a bit more planning, flexibility, and creativity than it did in the past. Here is a practical guide that can help you navigate the process.

Start with a financial checkup

Before you even start looking for a house, you'll need to assess your financial situation. You should first check your credit score, which is based on your past and present credit transactions. Having a good credit score is important because most mortgage lenders will use it to evaluate your creditworthiness. A higher score will often help you obtain a lower interest rate for a mortgage, which could save you thousands of dollars over the life of your loan. If you discover that you need to increase your credit score, focus on paying your bills on time and reducing high-interest debt.

You should also consider saving for a healthy down payment, since putting more money down can reduce the amount you'll need to borrow and may make your offer more attractive to a seller. Try implementing the following strategies to help boost your down payment:

- Automate your savings so a portion of each paycheck goes directly into a home fund.

- Examine your budget and focus on reducing your discretionary spending.

- Boost your savings with windfalls from tax refunds, bonuses, or gifts from family members.

Explore first-time homebuyer programs

There are numerous mortgage programs geared specifically towards first-time homebuyers that can significantly reduce the upfront cost of buying a home. Government programs, such as FHA loans, often require lower down payments. Local and state programs may offer grants, down payment assistance, or reduced interest rates.

Seek out alternative financing options

Buyers can also consider alternative financing options to help lower their interest rates. Here are some that may be worth looking into:

- Adjustable-rate mortgage (ARM) also referred to as a variable-rate mortgage, typically has a fixed interest rate at the beginning of the loan, which then adjusts annually or biannually for the remainder of the loan term. The initial interest rate on an ARM is generally lower than the rate on a traditional fixed-rate mortgage, which will result in a lower monthly mortgage payment.

- Temporary buydown provides the buyer with a lower interest rate on a fixed-rate mortgage during the beginning of the loan period (e.g., the first one or two years) in exchange for an upfront fee or higher interest rate once the buydown feature expires.

- Assumable mortgage allows a buyer to take over a seller's existing loan and loan terms and pay cash or take out a second mortgage to cover the remainder of the purchase price.

Look into other cost-saving opportunities

In addition to alternative financing, there are other ways to help lower the cost of buying a home. One option is to pay an upfront fee at closing, also known as points. By paying points, a buyer can reduce the interest rate, usually by around .25% per point, resulting in a lower mortgage loan payment. Another option, often referred to as a "future refi," allows a borrower to purchase a home at current interest rates, with the ability to refinance the loan to a lower rate at a later date. The cost to refinance is usually rolled into the new loan, depending on the lender and loan type.

Reconsider what "home" means

A first home doesn't need to be your forever home. Look into smaller properties that tend to be more affordable, such as condos, townhouses, or apartments. Are you priced out of a specific area? Consider emerging and up-and-coming neighborhoods where prices may be more affordable or be open to fixer-uppers if you are willing to invest time (and money) into home improvements.

You may even want to look into purchasing a home with someone else, such as a partner, sibling, or close friend, in order to share costs. While shared ownership can make homeownership possible sooner, it does require trust and clear communication, with clearly documented co-buying agreements, to help avoid future conflicts.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.