Inflation Protection for Investment Dollars

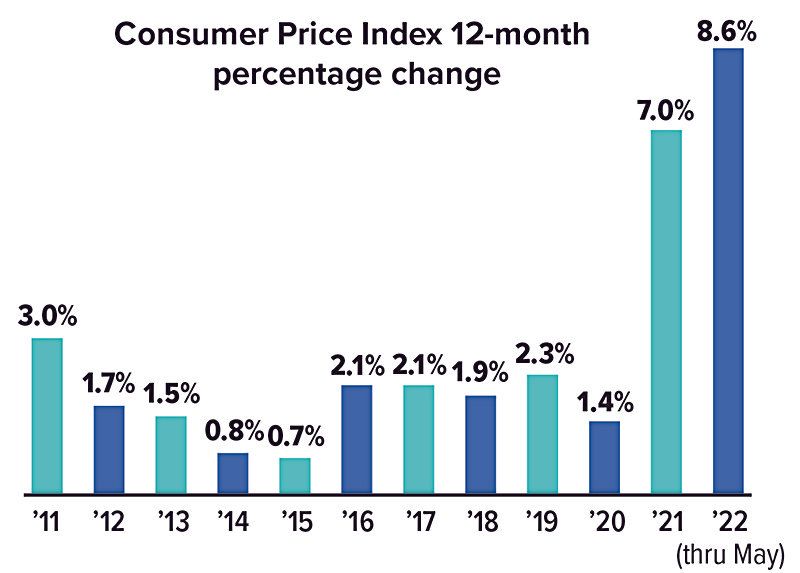

For the 12-month period ending in May 2022, the Consumer Price Index for All Urban Consumers (CPI-U) — the most widely used measure of inflation — increased 8.6%, the fastest pace in 40 years.(1)

The rate may trend downward as the Federal Reserve raises interest rates and supply-chain issues improve. But inflation is likely to be relatively high for some time.

High inflation not only hits consumers in the pocketbook for current spending, it also has a negative impact on the future purchasing power of fixed-income investments. For example, a hypothetical investment earning 5% annually would have a real return of –2.5% during a period of 7.5% annual inflation. This rate of return might be further reduced by taxes.

One way to help hedge your bond portfolio against inflation is by investing in Treasury Inflation-Protected Securities (TIPS).

How TIPS Fight Inflation

The principal value of TIPS is automatically adjusted twice a year to match any increases or decreases in the Consumer Price Index. If the CPI-U moves up or down, the Treasury recalculates your principal to reflect the change. A fixed rate of interest is paid twice a year based on the current principal, so the amount of interest may also fluctuate. Thus, you are trading the certainty of knowing exactly how much interest you'll receive for the assurance that your investment will maintain its purchasing power over time.

Like all Treasury securities, TIPS are guaranteed by the federal government as to the timely payment of principal and interest. If you hold TIPS to maturity, you will receive the greater of the inflation-adjusted principal or the amount of your original investment.

Pricing-In Protection

TIPS pay lower interest rates than equivalent Treasury securities that don't adjust for inflation. The breakeven inflation rate is the difference between the yield of TIPS and nominal (non-inflation-protected) Treasury securities with similar maturities. It is the premium the investor pays for inflation protection, as well as a market-based measure of expected inflation.

If inflation runs higher than expected, TIPS will earn a better return than nominal Treasury securities. If inflation runs below the breakeven rate, then TIPS have no clear advantage. However, the increased principal due to any level of inflation can still add to the value of your portfolio.

In some situations, TIPS can have negative interest rates that might produce a positive return after the principal is increased for inflation. For example, if a five-year TIPS offers a return of –0.5% while a five-year Treasury note offers a return of 2.5%, the 3% difference between these rates is the breakeven inflation rate. If inflation were to run at 4% over the five-year period, the TIPS would return 3.5% (4% – 0.5%) after adjustments for inflation, 1% higher than the return on the Treasury note.(2)

TIPS are sold in $100 increments and are available in maturities of 5, 10, and 30 years. As with all bonds, the return and principal value of TIPS on the secondary market will vary with market conditions, are sensitive to movements in interest rates, and may be worth more or less than their original cost. When interest rates rise, the value of existing TIPS will typically fall on the secondary market. Changing rates and secondary-market values should not affect the principal of TIPS held to maturity.

You must pay federal income tax each year on the interest income from TIPS plus any increase in principal, even though you won't receive the principal and interest until the bonds mature. For this reason, investors might consider holding TIPS in a tax-deferred account such as an IRA.

ERODING PURCHASING POWER

After an extended period of low inflation, consumer prices spiked in 2021 and 2022 due to supply and demand imbalances as the U.S. economy reopened.

(1) U.S. Bureau of Labor Statistics, 2022

(2) This hypothetical example of mathematical principles is used for illustrative purposes only. Rates of return will vary over time, particularly for long-term investments. Actual results will vary.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.