Mixing It Up: Asset Allocation and Diversification

Asset allocation and diversification are so fundamental to portfolio structure that it's easy to lose sight of these strategic tools as you track the performance of specific securities or the dollar value of your investments.

It might be worth considering how these strategies relate to each other and to the risk and potential performance of your portfolio.

Keep in mind that asset allocation and diversification are methods used to help manage investment risk; they do not guarantee a profit or protect against investment loss.

Establishing balance

Asset allocation refers to the mix of asset types in a portfolio — generally stocks, bonds, and cash alternatives. These asset classes have different growth and risk profiles and tend to perform differently under various market conditions. Stocks typically have higher long-term growth potential but are associated with greater volatility, while bonds tend to have moderate growth potential with less volatility. Cash alternatives usually have low growth potential but are the most stable of the three asset classes; however, if cash investments do not keep pace with inflation, they could lose purchasing power over time.

There is no right or wrong asset allocation. The appropriate allocation for you depends on your age, risk tolerance, time horizon, and specific goals. Younger investors might be comfortable with a more aggressive allocation heavily weighted toward stocks, because they have a longer time to recover from potential losses and may be willing to accept significant short- to medium-term drops in portfolio value in exchange for long-term growth potential. Older investors who are more concerned with preserving principal and those with near-term investment objectives, such as college funding, might prefer a more conservative allocation with greater emphasis on bonds and cash alternatives.

Adding variety

Diversification refers to holding a wide variety of securities within an asset class to help spread the risk within that class. For example, the stock portion of a portfolio could be diversified based on company size or capitalization (large cap, mid cap, and small cap). You could add international stocks, which tend to perform differently than domestic stocks. A well-diversified portfolio should include stocks across a broad range of industries and market sectors.

A portfolio's bond allocation might be diversified with bonds of different types and maturities. Corporate bonds typically pay higher interest rates than government bonds with similar maturities, but they are associated with a higher degree of risk. U.S. Treasury bonds are guaranteed by the federal government as to the timely payment of principal and interest. Foreign bonds could also increase diversification. Longer-term bonds tend to be more sensitive to interest rates; they typically offer higher yields than bonds with shorter maturities, but this has not been true since the unusual interest-rate increases that began in 2022.

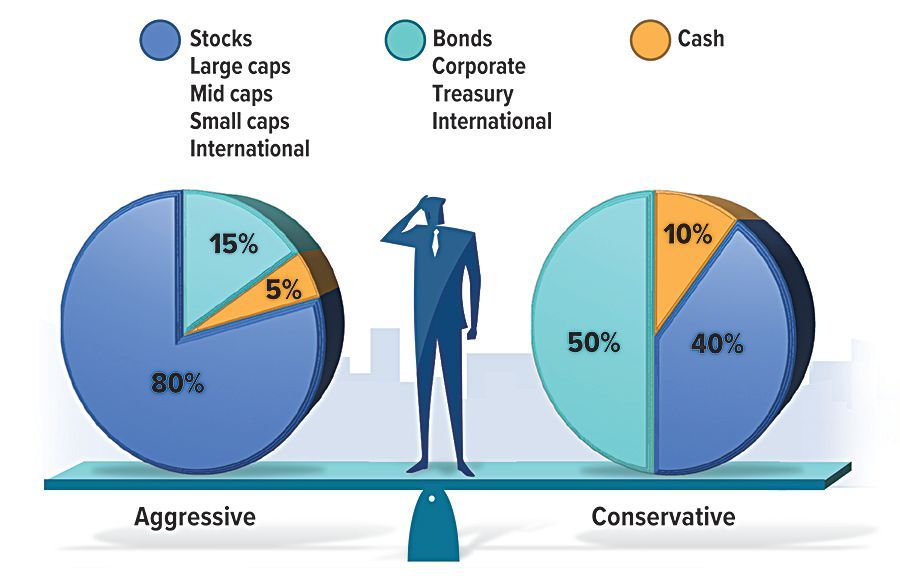

Sample Portfolios

This chart shows how aggressive and conservative portfolios could be diversified by dividing asset classes among different types of securities. The percentage of each type of security might vary widely depending on the investor's situation and preferences, and many investors may not hold all types of securities.

Staying on target

Once you have established an appropriate asset allocation and diversification strategy, it's important to periodically examine your portfolio to see how it compares to your targeted structure. Depending on the level of change, you may want to rebalance the portfolio to bring it back in line with your strategic objectives. Rebalancing involves selling some investments in order to buy others. Keep in mind that selling investments in a taxable account could result in a tax liability.

The principal value of stocks and bonds fluctuate with changes in market conditions. Shares of stock, when sold, and individual bonds redeemed prior to maturity may be worth more or less than their original cost. Concentrating in a particular industry or sector could expose your portfolio to significant levels of volatility and risk. Investing internationally involves additional risks, such as differences in financial reporting, currency exchange risk, and economic and political risk unique to the specific country or region. This may result in greater share price volatility. The principal value of cash alternatives may be subject to market fluctuations, liquidity issues, and credit risk; it is possible to lose money with this type of investment.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.