Charitable Gifts of Life Insurance

Life insurance can be an excellent tool for charitable giving.

Not only does life insurance allow you to make a substantial gift to charity but you may also benefit from tax rules that apply to gifts of life insurance.

Why gift life insurance?

Life insurance allows you to make a much larger gift to charity than you might otherwise be able to afford. Generally, the amount the charity will receive (the death benefit) is usually much greater than the cost to you (premium payments). As long as you continue to pay the premiums on the life insurance policy, the charity will receive the proceeds of the policy when you die. Since life insurance proceeds paid to a charity are not subject to income taxes, probate costs, and other expenses, the charity can count on receiving 100% of your gift.

What are the possible tax benefits?

Giving life insurance to a qualified charity also has certain income tax benefits. Depending on how you structure your gift, you may be able to take an income tax deduction of the premium payments.

Charitable income tax deductions may be available if the charity is named owner and beneficiary of an existing life insurance policy. You can generally deduct the lesser of your cost basis in the policy or the value of the policy at the time of the transfer to the charity. In addition, subsequent gifts to the charity to pay premiums may be eligible for charitable income tax deductions in the year the gifts are made. You may also receive a charitable income tax deduction if you buy a new policy naming the charity as owner and beneficiary. Also, irrevocable gifts to charity are not subject to federal gift tax. There may also be estate tax benefits where either the policy is not included in your estate, or you receive a federal estate tax deduction.

Are there disadvantages to charitable gifting of life insurance?

Donating a life insurance policy to charity (or naming the charity as beneficiary on the policy) means that you have less wealth to distribute among your heirs when you die. This may discourage you from making gifts to charity. However, this problem is relatively simple to solve. You could consider buying another life insurance policy that will benefit your heirs instead of a charity.

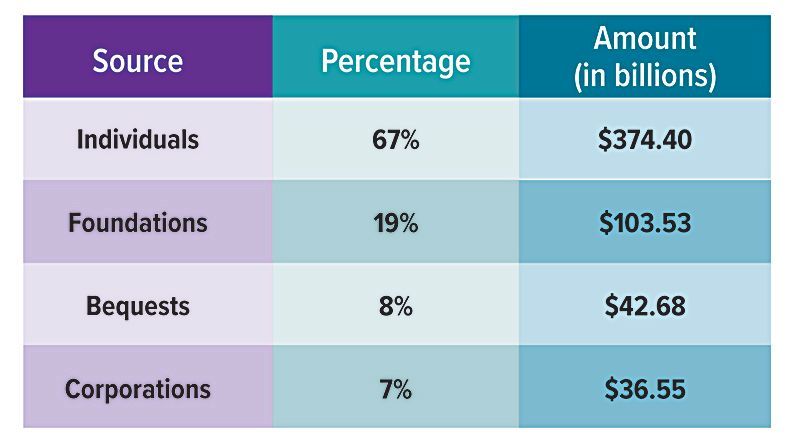

2023 Charitable Giving, by Source

In 2023, Americans gave $557.16 billion to charity.

How can life insurance be given to a charity?

The simplest way is to name a charity as beneficiary of your life insurance policy. Most policies allow you to name multiple beneficiaries, so you could split the death benefit between individuals, such as family members, and a charity. If the policy is a form of cash value life insurance, you still have access to the cash value of the policy during your lifetime. However, this type of charitable gift does not provide many of the income tax benefits of charitable giving, because you retain control of the policy during your life. When you die, the proceeds are included in your gross estate, although the full amount of the proceeds payable to the charity can be deducted from your gross estate.

You may donate an existing life insurance policy to charity. To do this, you must assign all ownership rights in the policy to the charity. You must also deliver the policy itself to the charity. By doing this, you give up all control of the life insurance policy. This strategy provides the full tax advantages of charitable giving because the transfer of ownership is irrevocable. You may be able to take an income tax deduction, and the policy may not be included in your gross estate when you die.

As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications. The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.