Key Retirement and Tax Numbers for 2026

Every year, the Internal Revenue Service announces cost-of-living adjustments that affect contribution limits for retirement plans and various tax deduction, exclusion, exemption, and threshold amounts.

Here are some of the key adjustments for 2026.

Estate, gift, and generation-skipping transfer tax

- The annual gift tax exclusion (and annual generation-skipping transfer tax exclusion) for 2026 is $19,000, unchanged from 2025.

- The gift and estate tax basic exclusion amount (and generation-skipping transfer tax exemption) for 2026 is $15,000,000, up from $13,990,000 in 2025.

Standard deduction

A taxpayer can generally choose to itemize certain deductions or claim a standard deduction on the federal income tax return. In 2026, the standard deduction is:

- $16,100 (up from $15,750 in 2025) for single filers or married individuals filing separate returns

- $32,200 (up from $31,500 in 2025) for married joint filers

- $24,150 (up from $23,625 in 2025) for heads of households

The additional standard deduction amount for the blind and those age 65 or older in 2026 is:

- $2,050 (up from $2,000 in 2025) for single filers and heads of households

- $1,650 (up from $1,600 in 2025) for all other filing statuses

Special rules apply for an individual who can be claimed as a dependent by another taxpayer.

The One Big Beautiful Bill Act, signed into law in July 2025, introduced a new senior deduction of $6,000 for taxpayers filing individually who are age 65 or older for tax year 2026. A deduction of up to $12,000 may be claimed by married couples filing jointly if they are both age 65 or older. This deduction is stacked on top of the standard deduction and additional deduction for the blind and those age 65 or older or on top of itemized deductions.

IRAs

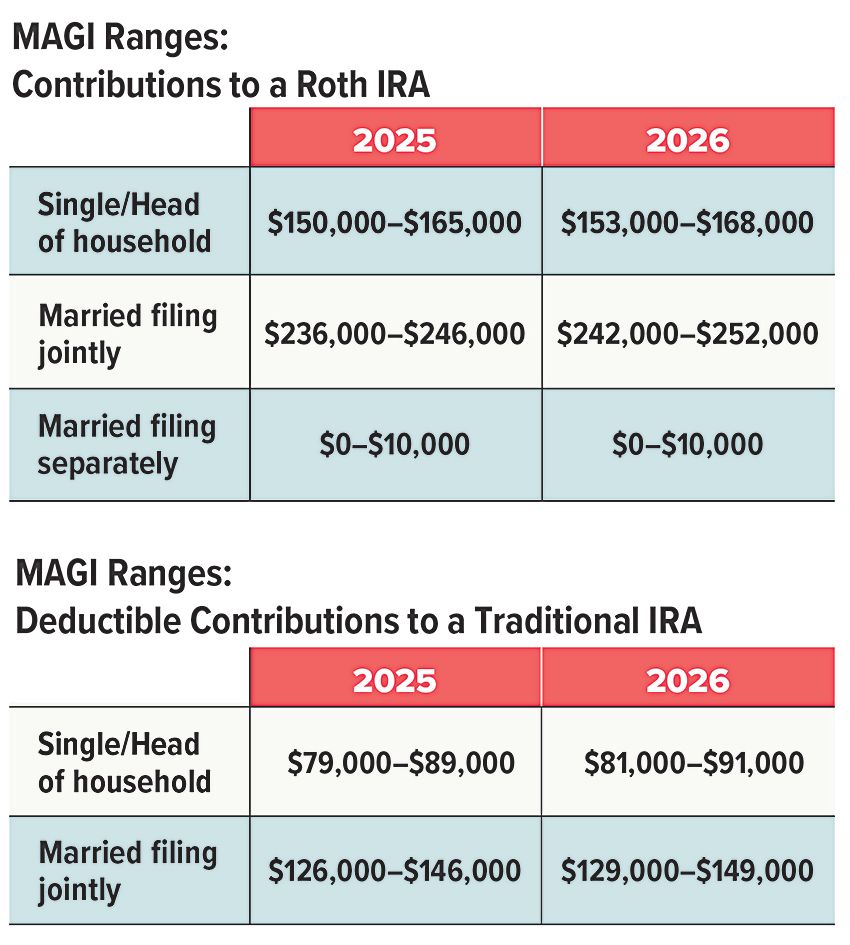

The combined annual limit on contributions to traditional and Roth IRAs is $7,500 in 2026 (up from $7,000 in 2025), with individuals age 50 or older able to contribute an additional $1,100 in 2026 (up from $1,000 in 2025). The limit on contributions to a Roth IRA phases out for certain modified adjusted gross income (MAGI) ranges (see table). For individuals who are active participants in an employer-sponsored retirement plan, the deduction for contributions to a traditional IRA also phases out for certain MAGI ranges (see table). The limit on nondeductible contributions to a traditional IRA is not subject to phaseout based on MAGI.

Employer-sponsored retirement plans

- Employees who participate in 401(k), 403(b), and most 457 plans can defer up to $24,500 in compensation in 2026 (up from $23,500 in 2025); employees age 50 or older can defer up to an additional $8,000 in 2026 (up from $7,500 in 2025). For employees ages 60 to 63, the additional deferral limit is $11,250 for 2026 (unchanged from 2025).

- Employees participating in a SIMPLE retirement plan can defer up to $17,000 in 2026 (up from $16,500 in 2025), and employees age 50 or older can defer up to an additional $4,000 in 2026 (up from $3,500 in 2025), with an increase to $5,250 in 2026 (unchanged from 2025) for ages 60 to 63.

Kiddie tax: child's unearned income

Under the kiddie tax, a child's unearned income above $2,700 in 2026 (unchanged from 2025) is taxed using the parents' tax rates.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.