It's Complicated: Inheriting IRAs and Retirement Plans

The SECURE Act of 2019 dramatically changed the rules governing how IRA and retirement plan assets are distributed to beneficiaries.

The new rules, which took effect for account owner deaths occurring in 2020 or later, are an alphabet soup of complicated requirements that could result in big tax bills for many beneficiaries.

RMDs and RBDs

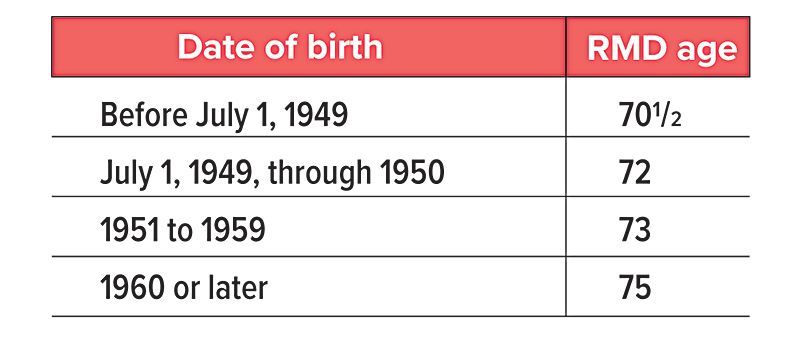

IRA owners and, in most cases, retirement plan participants must start taking annual required minimum distributions (RMDs) from their non-Roth accounts by April 1 following the year in which they reach RMD age (see table). This is known as their required beginning date (RBD).

Likewise, beneficiaries must take RMDs from inherited accounts (including, in most cases, Roth accounts). The timing and amount of an individual beneficiary's RMDs depend on several factors, including the relationship of the beneficiary to the original account owner and whether the original owner had reached the RBD.

Three key points apply to both owners and beneficiaries: (1) individuals must pay income taxes on the taxable portion of any distribution, (2) the larger the RMD, the higher the potential tax burden, and (3) failing to take the required amount generally results in an additional excise tax.1

The age that determines an account owner's RBD depends on the account owner's date of birth.

Spouse as sole beneficiary

Spouses who are sole beneficiaries have the most options for managing inherited accounts. By default, a surviving spouse beneficiary is treated as what's known as an eligible designated beneficiary (EDB) with certain advantages (see next section, "EDBs and DBs"). And if the deceased spouse died before the RBD, a surviving spouse EDB who is the sole owner can wait until the year the deceased would have reached RMD age to begin distributions.

Alternatively, a surviving spouse who is the sole owner can generally roll over the inherited account to their own account or elect to be treated as the account owner (rather than as an EDB). In these cases, the rules for account owners would apply. However, there is a potential drawback to this move: if the surviving spouse is younger than 59½, a 10% early distribution penalty may apply to subsequent withdrawals unless an exception applies.

EDBs and DBs

The SECURE Act separated other individual beneficiaries into two groups: EDBs and designated beneficiaries (DBs). EDBs are spouses and minor children of the deceased, those who are not more than 10 years younger than the deceased, and disabled and chronically ill individuals. DBs are essentially everyone else, including adult children and grandchildren.

EDBs have certain advantages over DBs. If the account owner dies before the RBD, an EDB is able to spread distributions over their own life expectancy. If the account owner dies on or after the RBD, an EDB may spread distributions over either their own life expectancy or that of the original account owner, whichever is more beneficial.2

By contrast, DBs are required to liquidate inherited assets within 10 years, which could result in unanticipated and hefty tax bills. If the account owner dies before the RBD, the beneficiary can leave the account intact until year 10. If the owner dies on or after the RBD, a DB must generally take annual RMDs based on their own life expectancy in years one through nine, then liquidate the account in year 10.

Other considerations

Work-sponsored retirement plans are not required to offer all distribution options; for example, an EDB may be required to follow the 10-year rule. However, both EDBs and DBs may roll eligible retirement plan assets into an inherited IRA, which may offer more options for managing RMDs.

This is just a broad overview of the complicated new rules as they apply to individual beneficiaries. If an account has multiple designated beneficiaries, or if a beneficiary is an entity such as a trust, charity, or estate, other rules apply. Beneficiaries should seek the assistance of an estate-planning attorney before making any decisions.

(1) The IRS has waived this tax as it applies to the DB 10-year rule through 2024.

(2) An inherited account must be liquidated 10 years after an EDB dies or a minor child EDB reaches age 21.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.