Is It Time to Declare Your Financial Independence?

No matter how much money you have or which life stage you're in, becoming financially independent starts with a dream.

Maybe you want to finally pay off the mountain of debt you've accumulated or stop relying on someone else for financial support. Or perhaps your dream is to retire early so you can spend more time with your family, travel the world, or open your own business. Financial independence, however you define it, is freedom from the financial obstacles that are keeping you from living life on your own terms.

Envision the future

If you were to become financially independent, what would change? Would you spend your time differently? Live in another place? What would you own? Would you work part time? Ultimately, it's up to you to define the life you want to live. It's your dream, so there's no wrong answer.

Work at it

Unless you're already wealthy, you may have had moments when winning the lottery seemed like the only way to become financially secure. But your path to financial independence isn't likely to start at the lottery counter of your local convenience store.

Though there are many ways to become financially independent, most of them require hard work. And retaining wealth isn't necessarily easy, because wealth may not last if spending isn't kept in check. As income rises, lifestyle inflation could slow, or even reverse, your progress. Becoming — and remaining — financially independent requires diligently balancing earning, spending, and saving.

Earn more

No matter which goals you're pursuing, the wider the gap between your income and expenses, the shorter the path to financial independence. The more you can earn, the more you can potentially save. This might mean finding a job with a higher salary, working an extra job, or working part time in retirement. And a job is just one source of income. If you're resourceful and able to put in extra hours, you may also be able to generate regular income in other ways — for example, renting out a garage apartment or starting a side business.

Spend wisely

Look for opportunities to reduce your spending without affecting your quality of life. For the biggest impact, focus on reducing your largest expenses, such as housing, food, and transportation. Practicing mindful spending can also help you free up more money to save. Before you buy something nonessential, think about how important it is to you and what value it brings to your life so that you don't end up with a garage, attic, or storage unit filled with regrettable purchases.

Save aggressively

Set a wealth accumulation goal and then prioritize saving. Of course, if you have a substantial amount of debt, saving may be somewhat curtailed until that debt is paid off. Take simple steps such as choosing investments that match your goals and time frame, and paying yourself first by automatically investing as much as possible in a retirement savings plan.

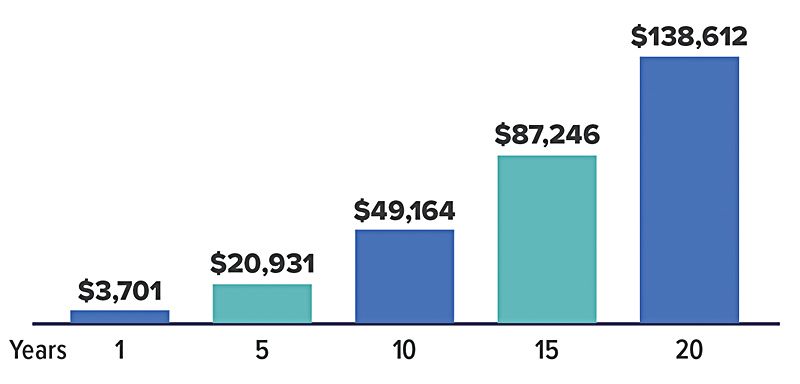

Investing for a Goal

Here's a hypothetical example showing how a $300 monthly investment would grow over time, assuming a 6% annual rate of return.

Time is an important ally in the quest for financial independence, so it would be wise to start saving as early as possible and build your nest egg over time. (Note that all investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.)

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.